- By 2030, up to 84% of BEV sales may have non-NCx (eg. LFP) cells, a change from near 0% in EU and North American markets today. This shift is driven by the inherent advantages of LFP over NCx chemistries in terms of cost, safety, reliability, and ESG.

- The volumetric and gravimetric density for cost tradeoff has reached a point where the same envelope for cells can be used for different BEV segments. Announcements of unified BEV platforms having different chemistry options by Tesla, VW, and Stellantis for high-volume BEVs will create significant Non-NCx markets.

- This will incentivize cell manufacturers to offer both NCx and non-NCx products where they have traditionally preferred only one.

Introduction

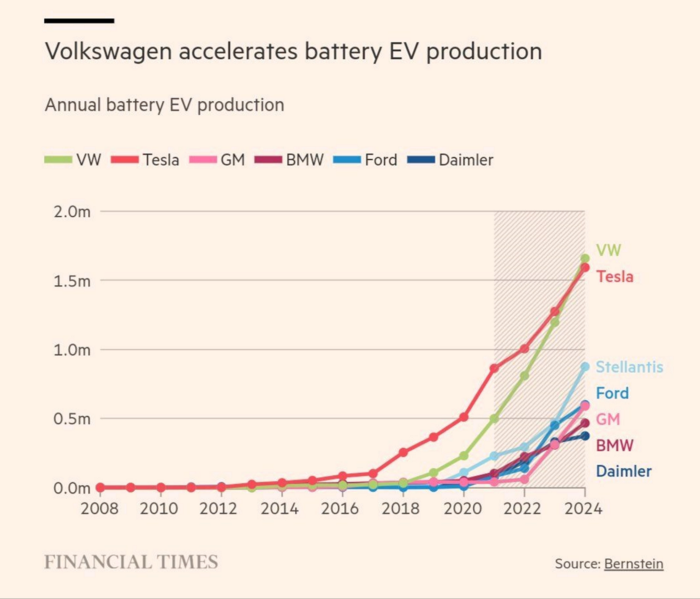

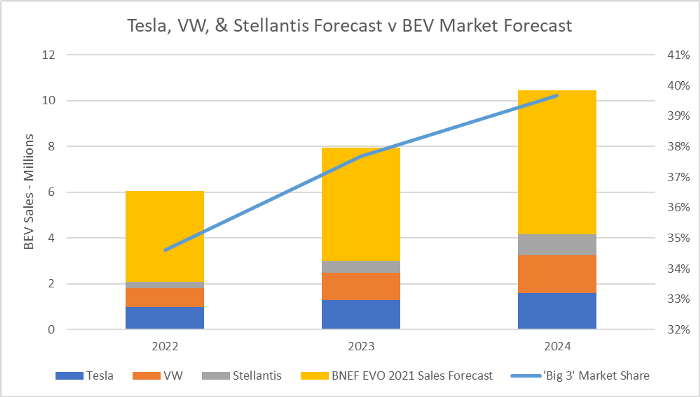

Tesla, VW, and Stellantis all held a battery, power, and EV day, respectively, in 2020 and 2021. While this is nothing new for Tesla, VW and Stellantis outlined plans to achieve ambitious electrification goals which include non-NCx chemistries. The most significant common themes among the three: a unified BEV platform and a multi-chemistry approach. This design is intended to drive down costs and produce profitable, low-cost, high-volume, and ESG compliant BEVS. This is significant because these three OEMs may produce four out of every ten BEVs in the world by 2024:

Financial Times

Ratel Consulting Analysis [1]

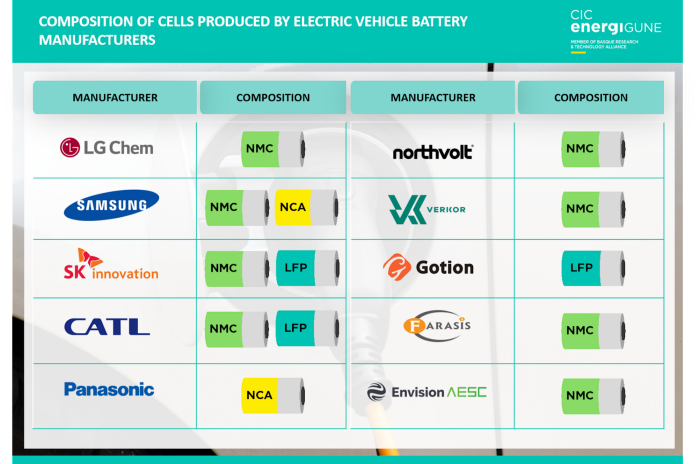

While this strategy may be good for the OEMs who will implement it, it may also be punitive for their battery suppliers. Most large cell suppliers have exclusively or heavily favored a specific chemistry. The EU and USA have almost exclusively been NCx markets for EVs dominated by Panasonic, LG Chem, AESC, and Samsung. Multi-chemistry platforms that include non-NCx will force these companies and others to expand their offerings to their customers’ needs or lose out on the growth potential of mass market BEVs.

CIC energiGUNE

We will examine the market impact of multi-chemistry platforms as well as the strategies and technologies that can give cell manufacturers the edge to maintain market share and growth prospects with multi-chemistry customers. Sodium-ion batteries fit the general definition of non-NCx however no official announcement has been made by any major OEM to use them in BEVs. While this potentially low cost chemistry holds promise we will omit it from this analysis.

Market & Forecast

Tesla, VW, and Stellantis all revealed their cathode chemistry by segment at their respective battery/power/EV days in 2020 and 2021:

Tesla Battery Day 2020

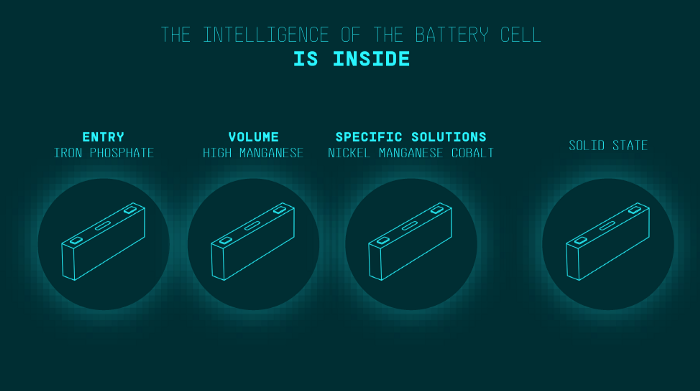

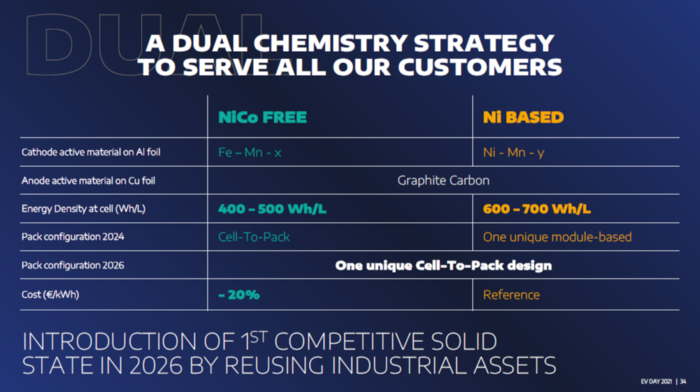

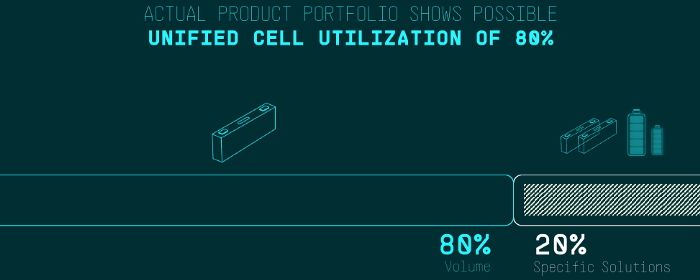

VW Power Day 2021

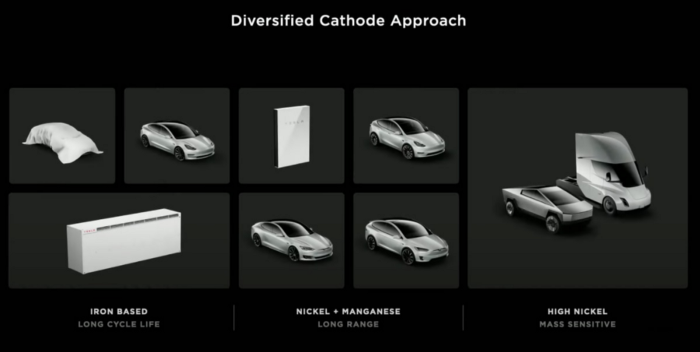

Stellantis EV Day 2021

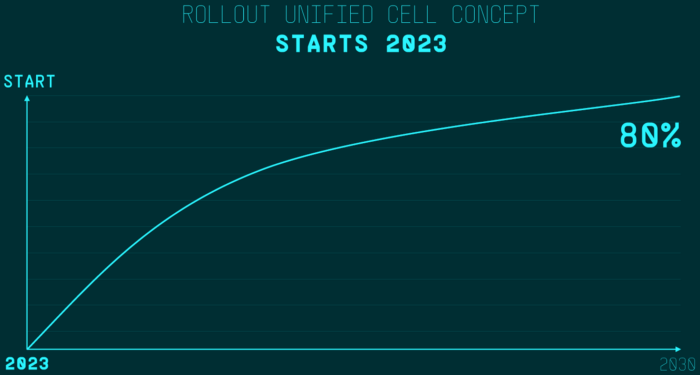

Based on historic ICE sales segmentation [2] and early growth indicators of lower-cost BEVs, we are assuming that 84% of BEV sales will have non-NCx cells resulting in 79% of deployed capacity by GWh [3] by 2030. This assumption is validated by VWs own projection of 80% by 2030 and starting in 2023:

A recent announcement by CATL for an 80 GWh North American factory that will produce LFP cells for BEVs further demonstrates cell makers adapting to OEMs electrification plans.

Business Strategy

From lab to market, cathode chemistries are not fungible which is why major cell manufacturers have typically favored one chemistry. LFP cathode suppliers are typically different from NCx cathode suppliers [4]. At a fundamental level LFP is more hygroscopic, necessitating different manufacturing tolerances on humidity from NCx.

In order to become a multi-chemistry manufacturer there are organic and non-organic options. LG Chem, a leader in the NCM market, formally announced they will be developing LFP for EV in January 2022. This organic option works well for them as they have abundant resources and a head start on R&D based on their statements. However, bringing a new chemistry to market from scratch can take up to five years which, if started today, would be 2027 and years behind the launch of multi-chemistry platforms.

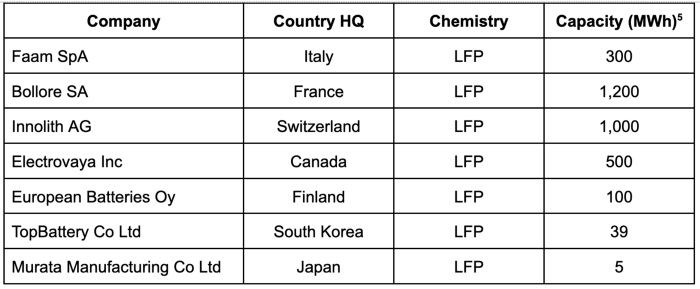

Non-organic options like acquisition and licensing have shorter go-to-market paths. However, licensing technology for a specific cathode chemistry may not be a practical option for a number of reasons, primarily because a cell manufacturer is not going to hand over trade secrets to a future competitor. Acquisition of small to medium sized non-NCx manufacturers is far more likely. The advantages here are an existing product, a manufacturing footprint, and employees who are knowledgeable on both fundamentals and production. Reliance New Energy’s acquisition of Lithium Werks is an example of this strategy. The following is a list of potential targets:

Technology Strategy

While acquisition and/or development of new chemistries is the first step in adapting to multi-chemistry platforms it will not be enough by itself. Cell manufacturers will still need to produce market leading products to compete in each chemistry market. For this we evaluated performance enhancement and/or cost savings, licensable technologies that are at a TRL 6 or higher. This generally indicates a technology that can be ready by when the major EV OEMs launch multi-chemistry unified platforms. We focused on manufacturing technologies and processes rather than materials. It is important that manufacturing technology partners be cathode agnostic, QuantumScape does a great job explaining why here. This segment is very chemistry agnostic and likely to appeal to a cell manufacturer building a more adaptable business model.

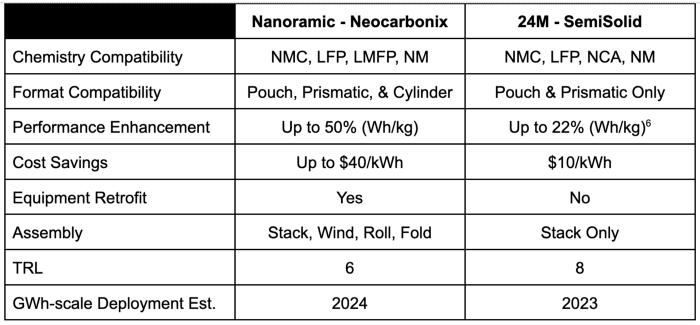

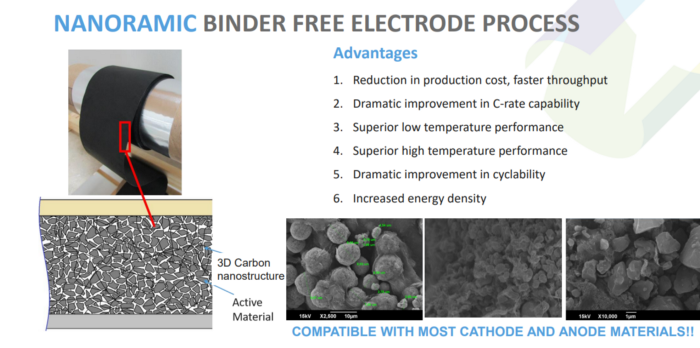

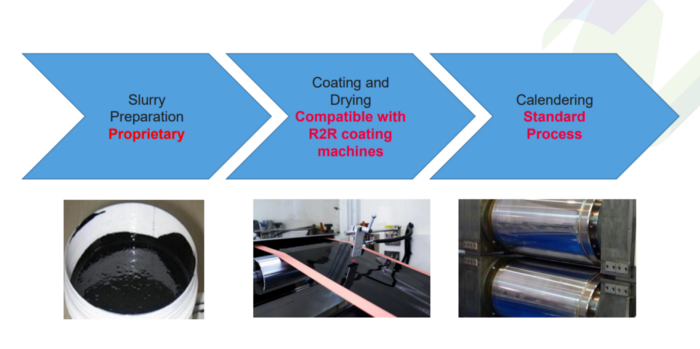

Nanoramic — Nanoramic Laboratories is an energy storage and advanced materials company spun out of MIT in 2009. Nanoramic’s proprietary battery technology, Neocarbonix® at the Core, enables Tier-I battery companies and automotive OEMs to achieve next-gen battery performance while using existing equipment and manufacturing processes. Neocarbonix at the Core replaces the plastic binder and toxic solvent used in conventional battery manufacturing with an advanced 3D nano-carbon binding structure using active carbon already present in electrode material.

Batteries made with Neocarbonix at the Core have higher active material loading, higher C-rate capability, lower resistance, and long cycle life, all at lower cost per kWh.

24M - Cambridge-based 24M has a licensable manufacturing platform. Invented in the MIT lab of Dr. Yet-Ming Chiang, SemiSolid electrodes use no binder, mixing electrolyte with active materials to form a clay-like slurry. The unique slurry allows the creation of ‘thick electrodes’ with less volume, mass and cost while enabling a simpler manufacturing process. 24M developed a cathode agnostic technology envisioning NMC for mobility and LFP for stationary but will benefit from LFPs growing presence in mobility.