- Battery Electric Vehicles (BEVs) are a growing but still niche segment in passenger vehicles because of unmet consumer demands for range, safety, and price.

- BEV OEMs are heavily invested in “Generation 4” battery technology to meet these demands, specifically solid-state batteries which may be a decade away from meaningful market penetration, and in the end may not be a panacea.

- Battery adjacent or ‘extra-cell technologies’ are available now or have shorter technology diffusion timelines that can produce results to meet consumer demands and propel mass market adoption for BEVs.

From Niche to Mass: Meeting Consumer Expectations

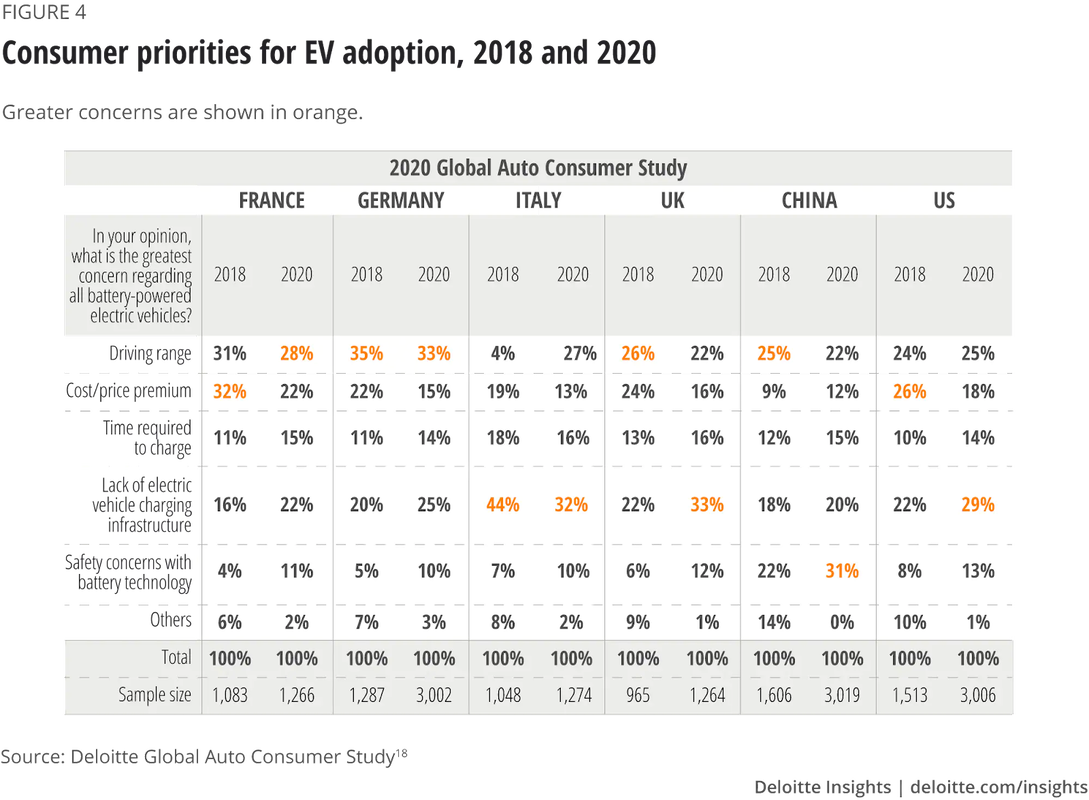

By the end of 2020, global passenger BEV market penetration was 2.7% and the global passenger BEV fleet stood at 0.6%. While this represents tremendous year-over-year growth, we are only just beginning to decarbonize road transport. Small, rich country governments like Norway have buoyed BEV sales with generous subsidies and consumer outreach akin to social programs, and have achieved >50% BEV market share. However this approach is not sustainable or viable in many large markets. A consumer-centric, market-based approach to mass-market BEV adoption will be necessary for countries to meet domestic and international GHG reduction targets. Consumers have made it clear that while they may be interested in purchasing a BEV as their next automobile, they are not wanting to make any compromises or pay more than they would for an Internal Combustion Engine (ICE) vehicle. Range, price, and safety are at the top of nearly every survey.

Addressing consumer demands for battery electric vehicles with battery technology appears logical and straightforward. The apparent solution to address these challenges is solid state battery technology. It ticks all of the boxes: an energy dense battery technology that can lower price, improve range, and is fire-retardant. OEMs like Volkswagen, Ford and BMW have invested hundreds of millions of dollars in companies developing solid-state batteries, possibly the largest external investment on a specific technology ever in the sector.

However, solid state battery technology may not help address consumer demands fast enough, or at all in some cases. A previous article from BatteryBits and a recent white paper by Battery Associates go into great detail on the commercialization challenges solid state technology faces and cite forecasts of only 7% market share by 2030. Meanwhile, a combination of other technologies has the potential to fulfill the promise held by solid state both sooner and cheaper.

While material technology like silicon-based anodes seek to approach the volume and gravimetric density of solid state, a number of extra-cell technologies are quietly helping BEVs meet consumer demands. Extra-cell technology can be defined as non battery material technologies that manufacture, manage, and utilize battery powered products, in this case BEVs. How batteries are made and how efficiently they are used throughout the life cycle can be just as impactful on product performance as the next generation of batteries themselves. This is an overlooked and underreported concept, as such the technologies analyzed in this paper were selected based on availability (or lack thereof) of relevant information.

Battery Capacity: Range Is The New Horsepower

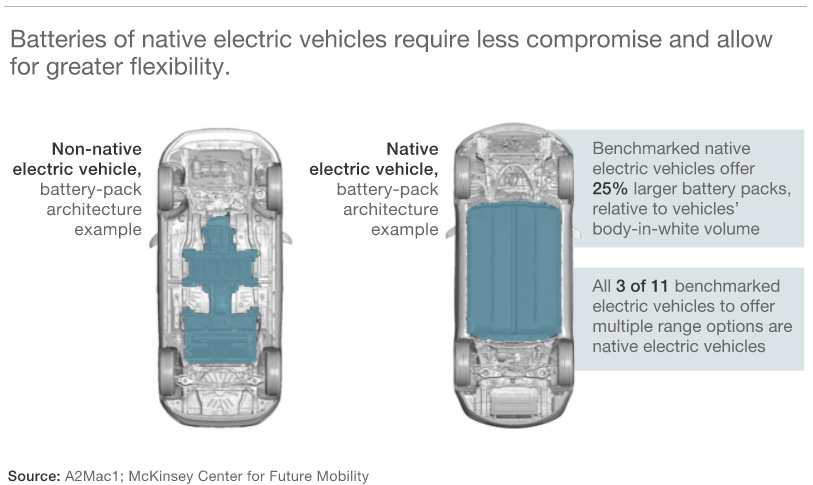

Range anxiety exists in the mind of the consumer, even if 87% of the population can get through the day with 74 miles of range. With the exception of Tesla and VW, auto OEMs have not invested in charging networks and as a result have little to no control over public charging density. What they do have control over is the range of the BEVs that they manufacture.

According to the Department of Energy (DOE), every gallon of gasoline is equivalent to ~33 kWh (GGE) giving the average 16 gallon gas tank the equivalent energy of a 533 kWh battery. Applying a 20% conversion efficiency puts equivalent energy at 107 kWh. Only a handful of high-end BEVs approach this capacity whereas every $25,000 Toyota Camry has a 16 gallon gas tank. This highlights the disparity of energy availability and the need for BEV energy efficient technologies.

Modern BEV powertrains evolved to a native (skateboard) platform as a result of clean sheet design. However, OEMs and tier-1 suppliers have borrowed subsystem technology from ICE vehicles without concern for energy efficiency. Heating a BEV in extreme cold can cut range by up to half and electric vehicle auxiliaries like power steering consumes almost as much energy as an air conditioner. BEV subsystems need a holistic approach to energy conservation and their own clean sheet redesign to be viewed more as a battery on wheels.

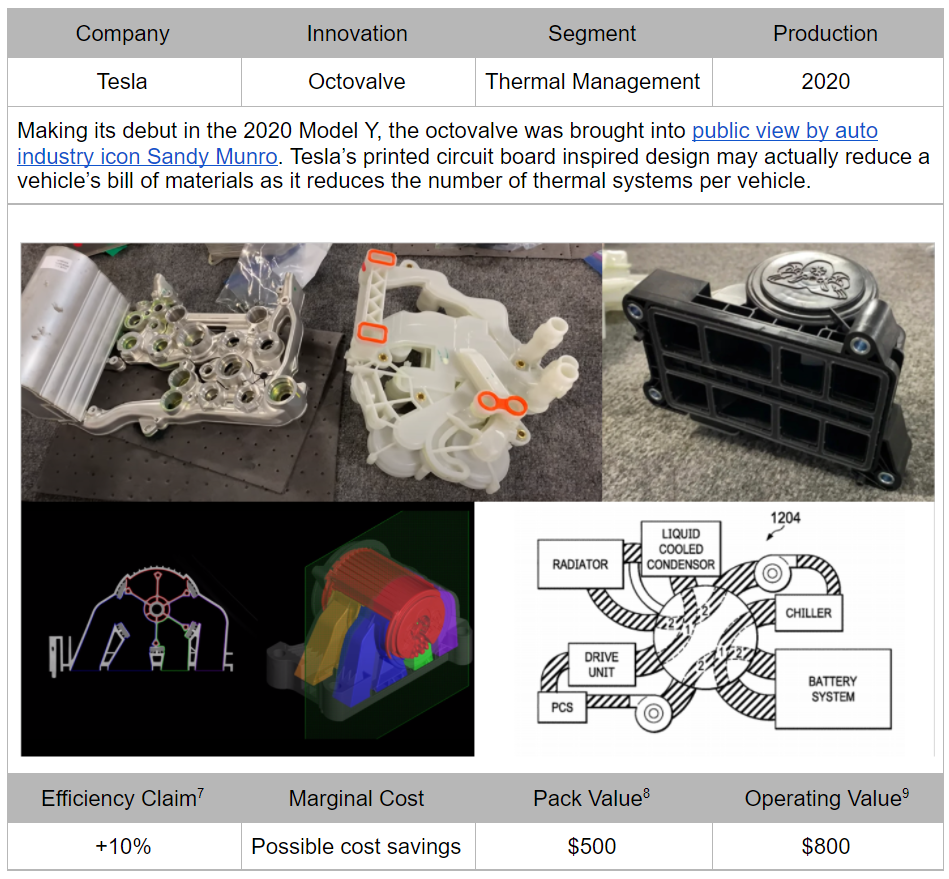

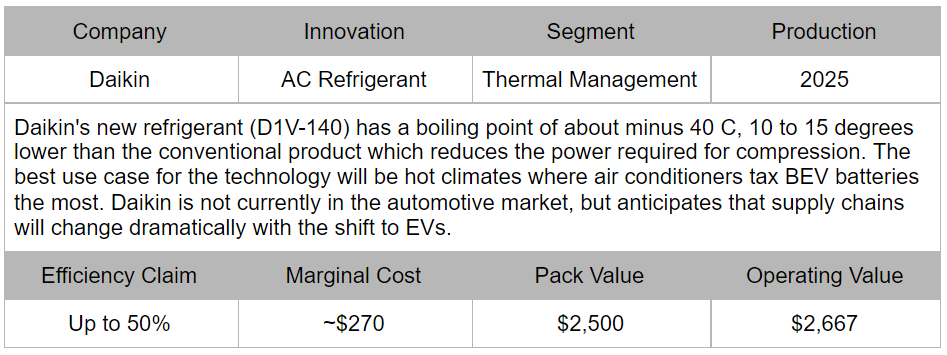

For this section, we looked at range enhancing technologies that have a significant measurable impact. There is a general scarcity of information in this area so we analyzed well publicized technologies that likely have the largest impacts. The selection of the below technologies is not an endorsement, but just select examples of tech that can work to solve these issues. It is important to note that these technologies are largely additive and independent in their nature so OEMs have the ability to pick and choose what configuration works best for them.

Safety: Perception Is Reality

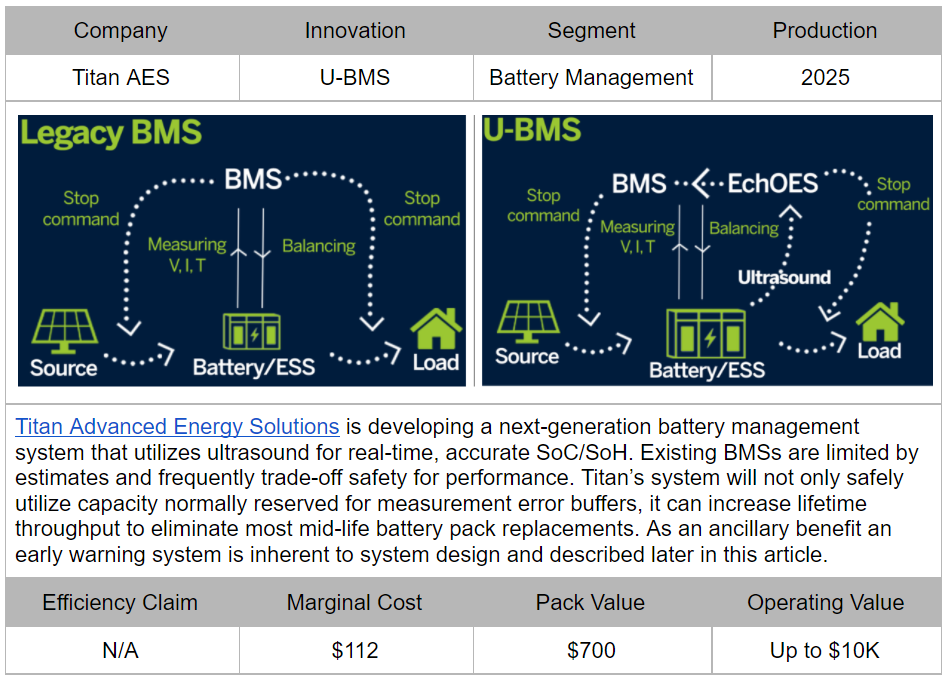

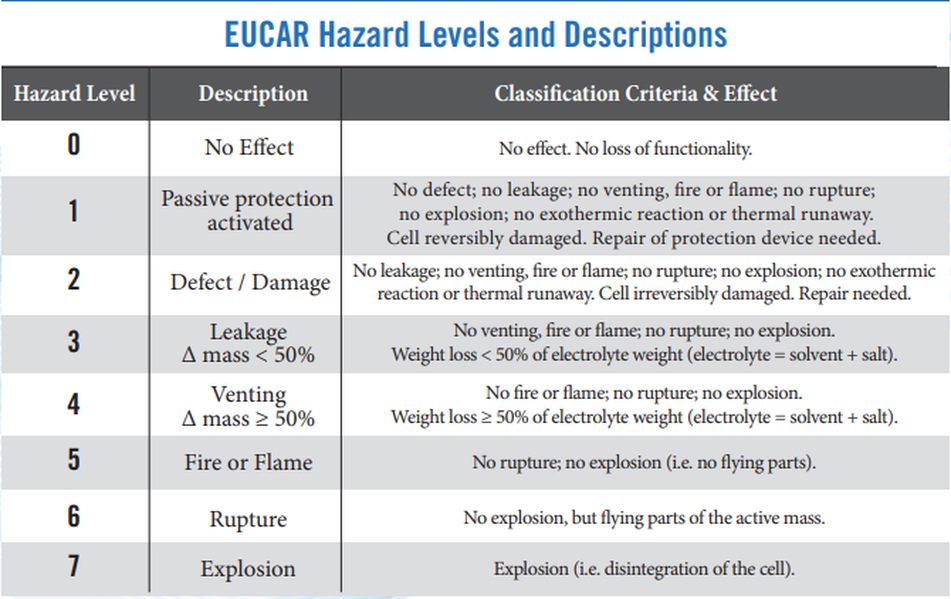

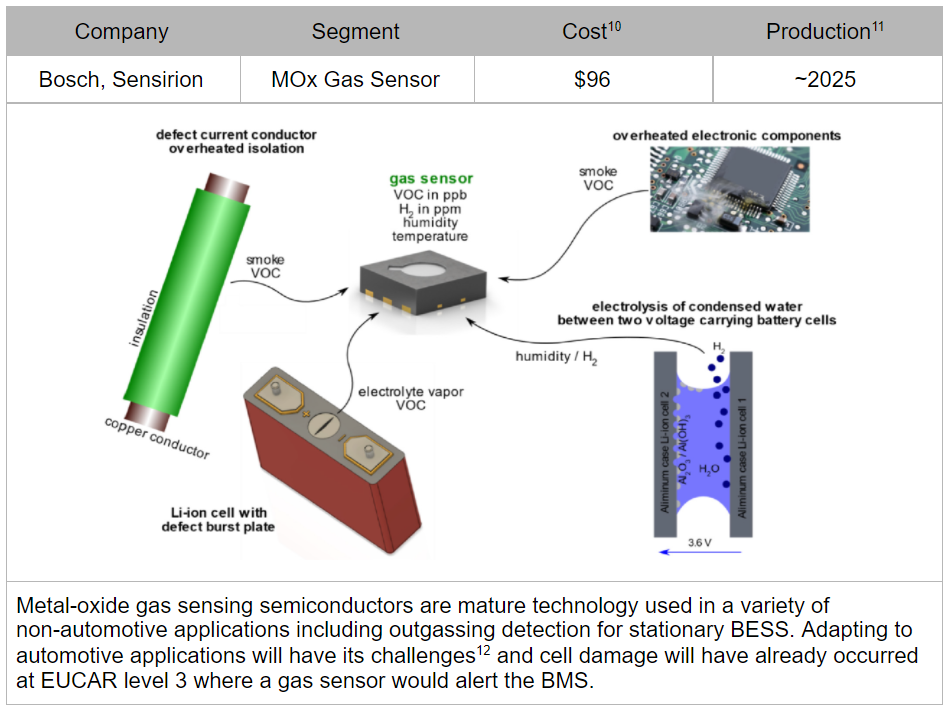

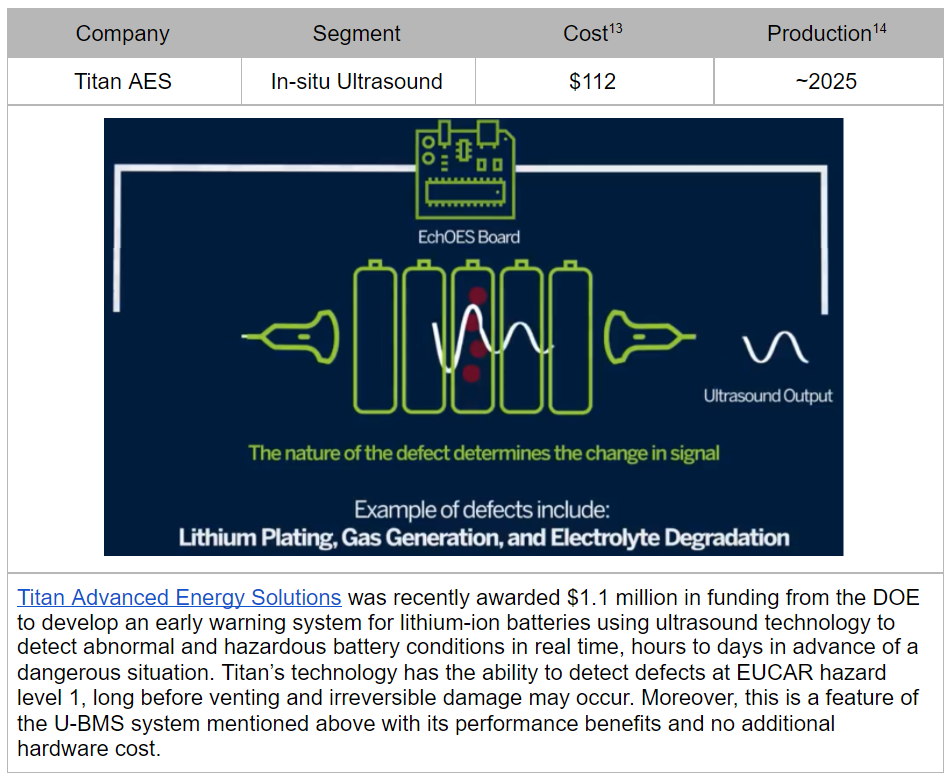

BEVs are safer than petrol cars per vehicle, per mile driven, in accident severity, and any other relevant metric. However this evidence is attenuated or ignored entirely when BEV batteries catch fire. To be fair, battery fires are violent, hard to control events that make for dramatic media content and sow distrust among consumers. To be more fair they are rare and the technologies that are being developed to mitigate or eliminate these events can remove one more hurdle to mass adoption well before solid state reaches the mass market. For this section we looked at sensor technologies that can help mitigate and possibly prevent BEV fires. As with the previous section there is a general scarcity of information in this area so we analyzed well publicized technologies that likely have the largest impacts.

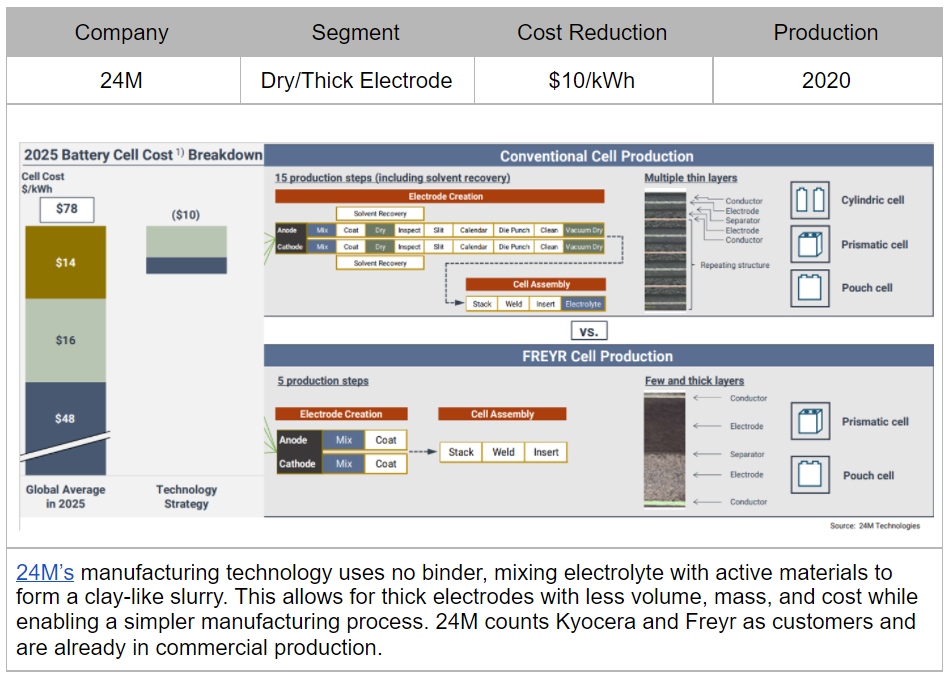

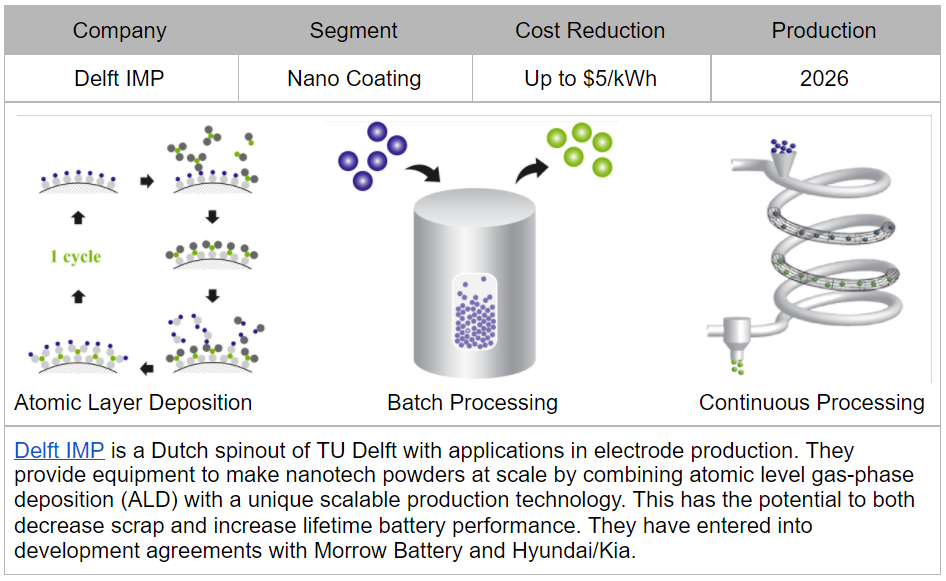

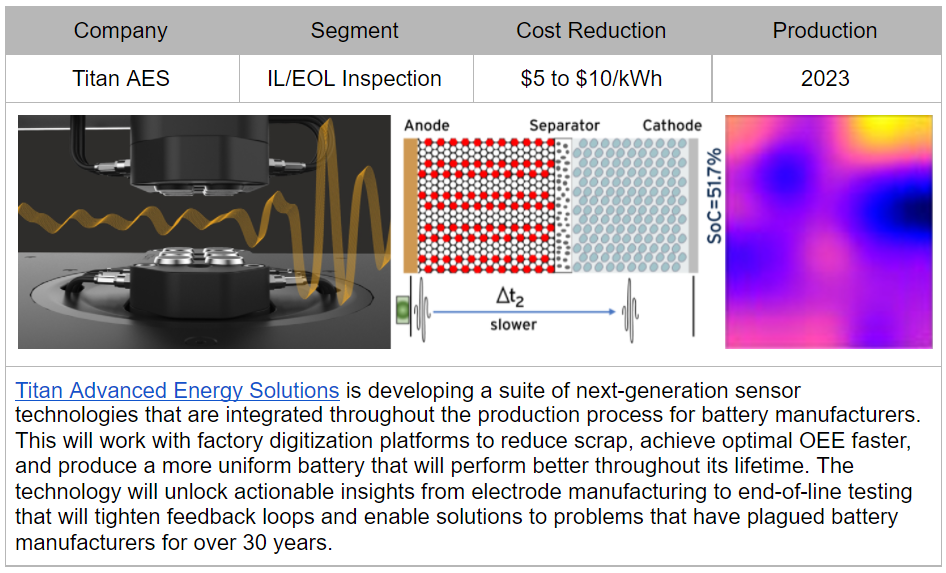

Price: Repeating The Learning Curve

A cost breakdown for a NMC 811 cell in a report issued by Roland Berger December 2020 shows a breakdown of material/non-material cost of 72% and 28%, respectively. While solid-state’s gravimetric density promises to pare down the larger material cost per kWh, improvements in manufacturing have the potential to make larger cost reductions with current chemistries.

As with the previous sections there is generally a scarcity of information in this area so we analyzed well publicized technologies that likely have the largest impacts.